The government is changing the sanctions for late submission and late payment to make them more consistent across taxes. The changes will initially apply to VAT and Income Tax Self Assessment (ITSA). New late submission penalties will affect those who fail to meet their obligations to provide returns and other information requested by HMRC on time.

Firstly, VAT interest rules are changing to align to those that currently exist in Income Tax Self-Assessment. HMRC have announced that the following changes will be made for VAT periods starting from 1 January 2023.

Late Payment Interest

Currently, Late Payment Interest (LPI) is not charged on late payments for VAT Returns.

It is planned that from 1st January 2023, it will be calculated at a rate of 2.5% + the Bank of England base rate. As the base rate currently 0.5%, the LPI would be 3%.

HMRC will charge late payment interest from the day your payment is overdue until the day it is paid in full. LPI will also apply to LSP and LPP penalties if paid aster 30 days.

VAT Repayment Interest

There is currently a 5% Repayment Supplement for falling to make repayment within 30 days of the claim. The payment or refund due is increased by 5% of the amount due to be paid or refunded or £50 whichever is greater.

Going forward, VAT Repayment Interest (RPI) will be paid at the Bank of England base rate

less 1% (with & minimum rate of 0.5%). HMRC will pay RPI on any tax due to be repaid to customers (from day +1 a repayment return is received until the date a repayment is issued)

Settling in Period

To give taxpayers time to get used to the changes, HMRC won’t be charging a late payment penalty for the first year from 1 January 2023 until 31 December 2023 if you pay in full within 30 days of your payment due date.

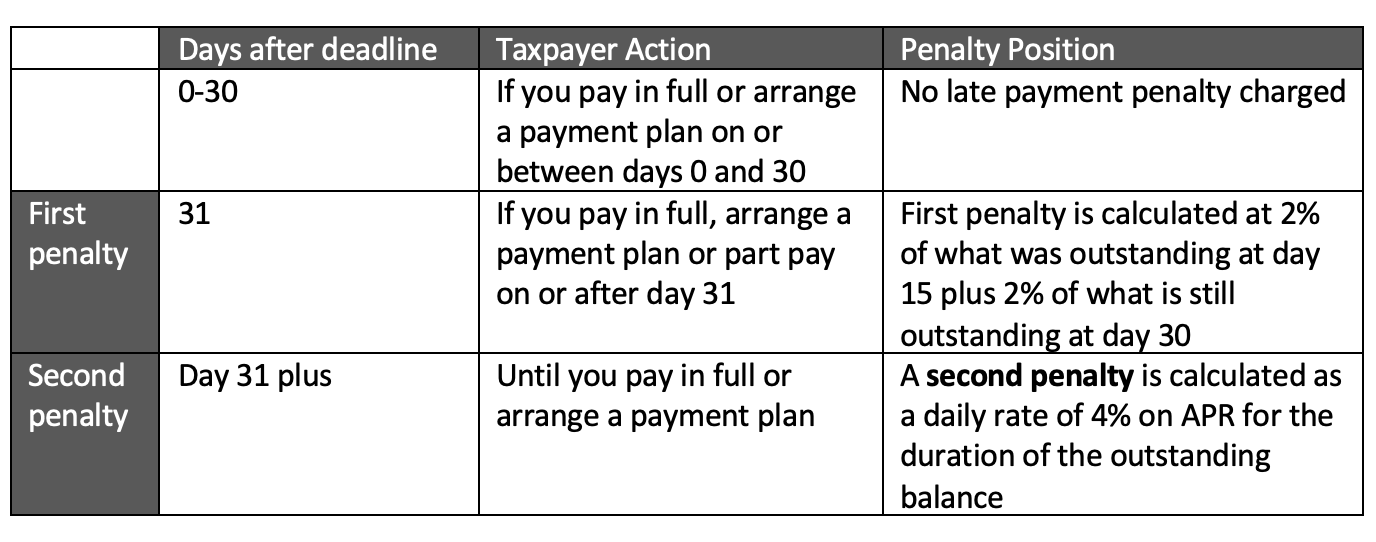

The below table shows how late payment penalties will work from 1 January 2023 to 31 December 2023

It should be noted that taxpayers will be able to appeal the penalty charges.

For more information, please follow this link to HMRC’s policy paper on Penalties for Late Submission.

Please get in touch with a member of the team if you need any further detail or help with the upcoming changes